by Sharron Parker | Jul 24, 2018 | Home Sellers

Every homeowner wants to make sure that they maximize their financial reward when selling their home, but how do you guarantee that you receive the maximum value for your house?

Here are two ways to ensure that you get the highest price possible.

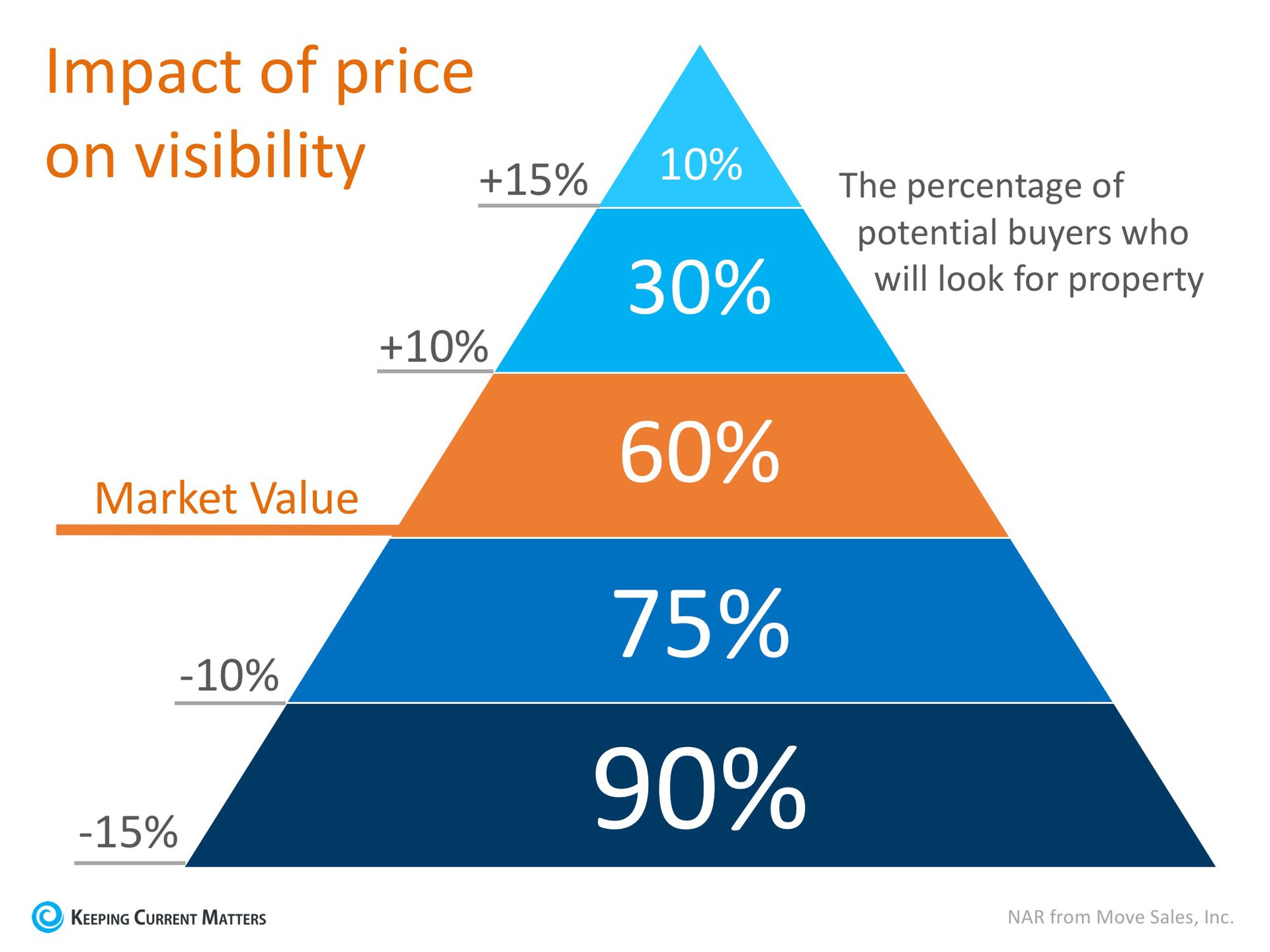

1. Price it a Little Low

This may seem counterintuitive, but let’s take a look at this concept for a moment. Many homeowners think that pricing their homes a little OVER market value will leave them with room for negotiation when, in actuality, it just dramatically lessens the demand for their houses (see chart below).

Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price their house so that demand for the home is maximized. By doing so, the seller will not be fighting with a buyer over the price but will instead have multiple buyers fightingwith each other over the house.

Realtor.com gives this advice:

“Aim to price your property at or just slightly below the going rate. Today’s buyers are highly informed, so if they sense they’re getting a deal, they’re likely to bid up a property that’s slightly underpriced, especially in areas with low inventory.”

2. Use a Real Estate Professional

This, too, may seem counterintuitive as the seller may think that he or she will make more money by avoiding a real estate commission. With this being said, studies have shown that homes typically sell for more money when handled by real estate professionals.

A study by Collateral Analytics, reveals that FSBOs don’t actually save any money, and in some cases may be costing themselves more, by not listing with an agent. The data showed that:

“FSBOs tend to sell for lower prices than comparable home sales, and in many cases below the average differential represented by the prevailing commission rate.”

The results of the study showed that the differential in selling prices for FSBOs, when compared to MLS sales of similar properties, is about 5.5%. Sales in 2017 suggest the average sales price was near 6% lower for FSBO sales of similar properties.

Bottom Line

Price your house at or slightly below the current market value and hire a professional. This will guarantee that you maximize the price you get for your house.

by Sharron Parker | Jul 23, 2018 | Home Buyers, Mortgage-Lending

- Many buyers are purchasing a home with a down payment as little as 3%.

- You may already qualify for a loan, even if you don’t have perfect credit.

- Take advantage of the knowledge of your local professionals who are there to help you determine how much you can afford.

by Sharron Parker | Jul 10, 2018 | Housing Market

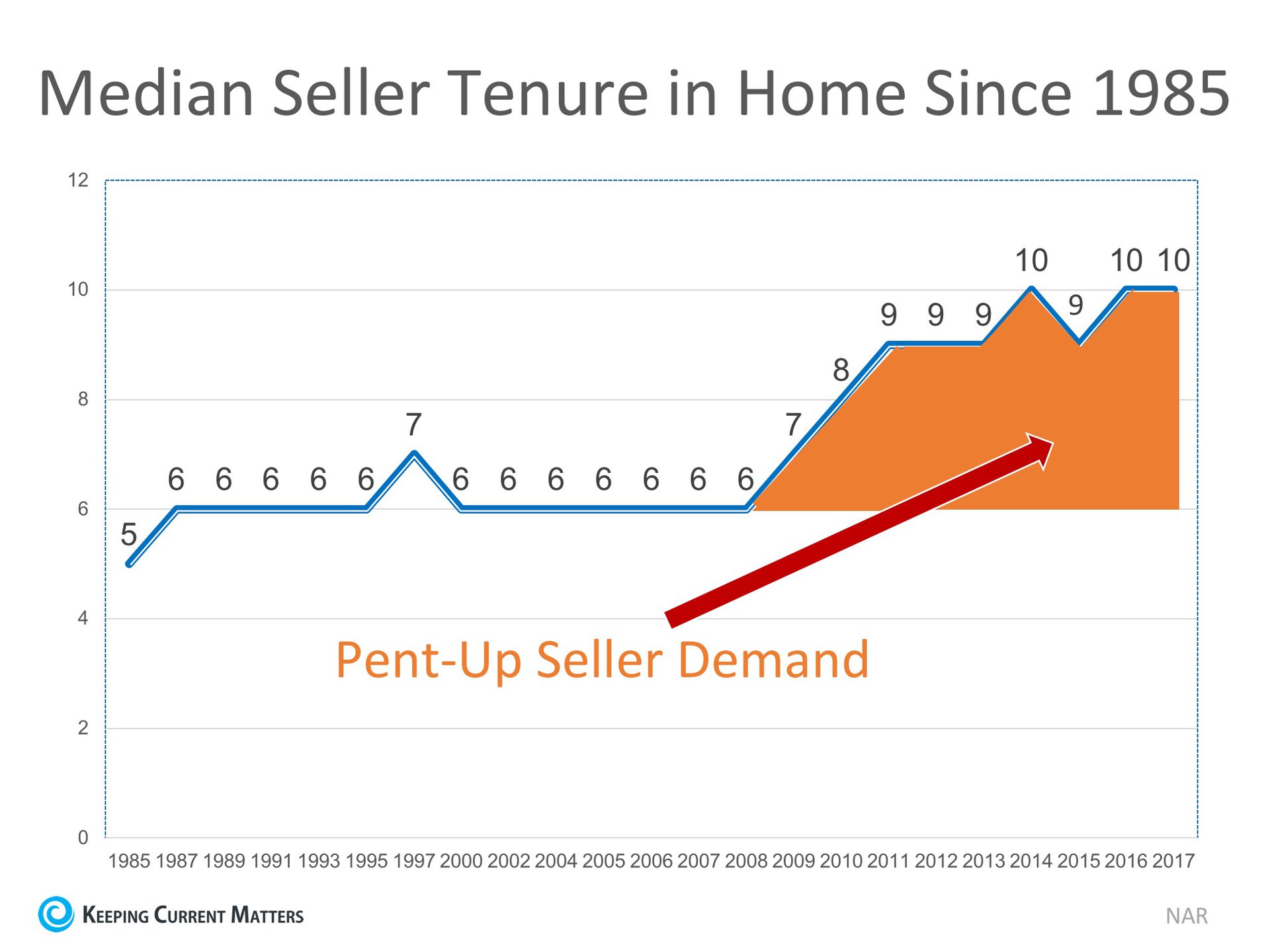

The National Association of Realtors (NAR) keeps historical data on many aspects of homeownership. One of their data points, which has changed dramatically, is the median tenure of a family in a home, meaning how long a family stays in a home prior to moving.

As the graph below shows, over the last twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2014, that average is almost ten years – an increase of almost 50%.

Why the dramatic increase?

The reasons for this change are plentiful!

The fall in home prices during the housing crisis left many homeowners in a negative equity situation (where their home was worth less than the mortgage on the property). Also, the uncertainty of the economy made some homeowners much more fiscally conservative about making a move.

With home prices rising dramatically over the last several years, 95.3% of homes with a mortgage are now in a positive equity situation, according to CoreLogic.

With the economy coming back and wages starting to increase, many homeowners are in a much better financial situation than they were just a few short years ago.

One other reason for the increase was brought to light by NAR in their 2018 Home Buyer and Seller Generational Trends Report. According to the report,

“Sellers 37 years and younger stayed in their home for six years…”

These homeowners, who are either looking for more space to accommodate their growing families or for better school districts to do the same, are likely to move more often (compared to typical sellers who stayed in their homes for 10 years). The homeownership rate among young families, however, has still not caught up to previous generations, resulting in the jump we have seen in median tenure!

What does this mean for housing?

Many believe that a large portion of homeowners are not in a house that is best for their current family circumstance; they could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple living in a one-bedroom condo planning to start a family.

These homeowners are ready to make a move, and since a lack of housing inventory is still a major challenge in the current housing market, this could be great news.

by Sharron Parker | Jul 9, 2018 | Housing Market

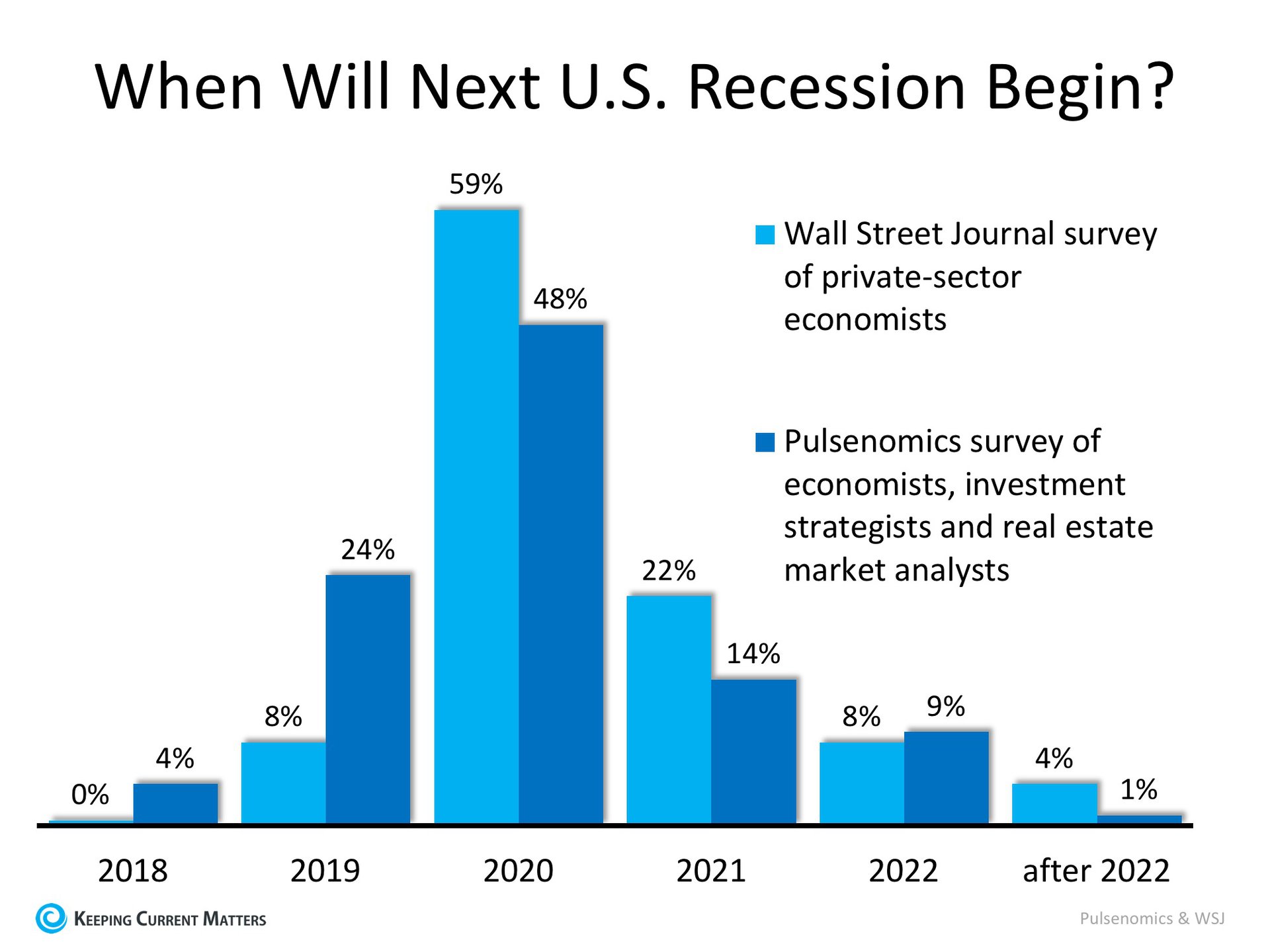

Economists and analysts know that the country has experienced economic growth for almost a decade. They also know that a recession can’t be too far off. A recent report by Zillow Research shed light on a survey conducted by Pulsenomics in which they asked economists, investment strategists and market analysts how they felt about the current housing market. That report revealed the possible timing of the next recession:

“Experts largely expect the next recession to begin in 2020.”

That timing concurs with a recent survey of economists by the Wall Street Journal:

“The economic expansion that began in mid-2009 and already ranks as the second-longest in American history most likely will end in 2020 as the Federal Reserve raises interest rates to cool off an overheating economy, according to forecasters surveyed.”

Here is a graph comparing the opinions of those surveyed by both the Wall Street Journal and Pulsenomics:

Recession DOES NOT Equal Housing Crisis

According to the Merriam-Webster Dictionary, a recession is defined as follows:

“A period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.”

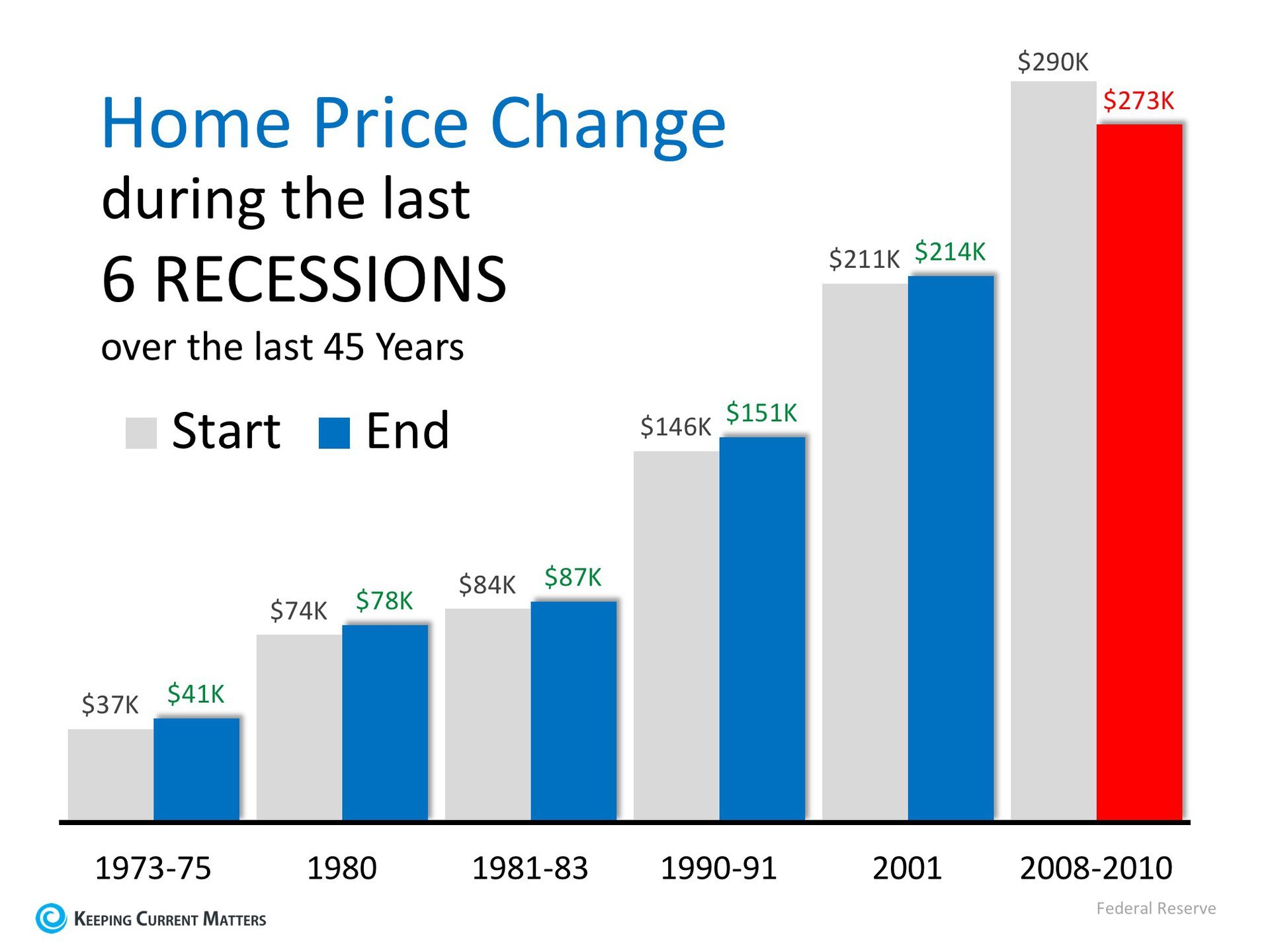

A recession means the economy has slowed down markedly. It does not mean we are experiencing another housing crisis. Obviously, the housing crash of 2008 caused the last recession. However, during the previous five recessions home values appreciated.

According to the experts surveyed by Pulsenomics, the top three probable triggers for the next recession are:

- Monetary policy

- Trade policy

- A stock market correction

A housing market correction was ranked ninth in probability. Those same experts also projected that home values would continue to appreciate in 2019, 2020, 2021 and 2022.

Others agree that housing will not be impacted like it was a decade ago.

Mark Fleming, First American’s Chief Economist, explained:

“If a recession is to occur, it is unlikely to be caused by housing-related activity, and therefore the housing sector should be one of the leading sources to come out of the recession.”

And U.S. News and World Report agreed:

“Fortunately – and hopefully – the history of recessions and current issues that could harm the economy don’t lead many to believe the housing market crash will repeat itself in an upcoming decline.”

Bottom Line

A recession is probably less than two years away. A housing crisis is not.

by Sharron Parker | Jul 6, 2018 | Housing Market

![Cost Across Time [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/wp-content/uploads/2018/07/03135215/20180706-KCM-ENG.jpg)

Some Highlights:

- With interest rates still around 4.5%, now is a great time to look back at where rates have been over the last 40 years.

- Rates are projected to climb to 5.1% by this time next year according to Freddie Mac.

- The impact your interest rate makes on your monthly mortgage cost is significant!

- Lock in a low rate now while you can!