by Sharron Parker | Aug 17, 2018 | Housing Market

Some are attempting to compare the current housing market to the market leading up to the “boom and bust” that we experienced a decade ago. They look at price appreciation and conclude that we are on a similar trajectory, speeding toward another housing crisis.

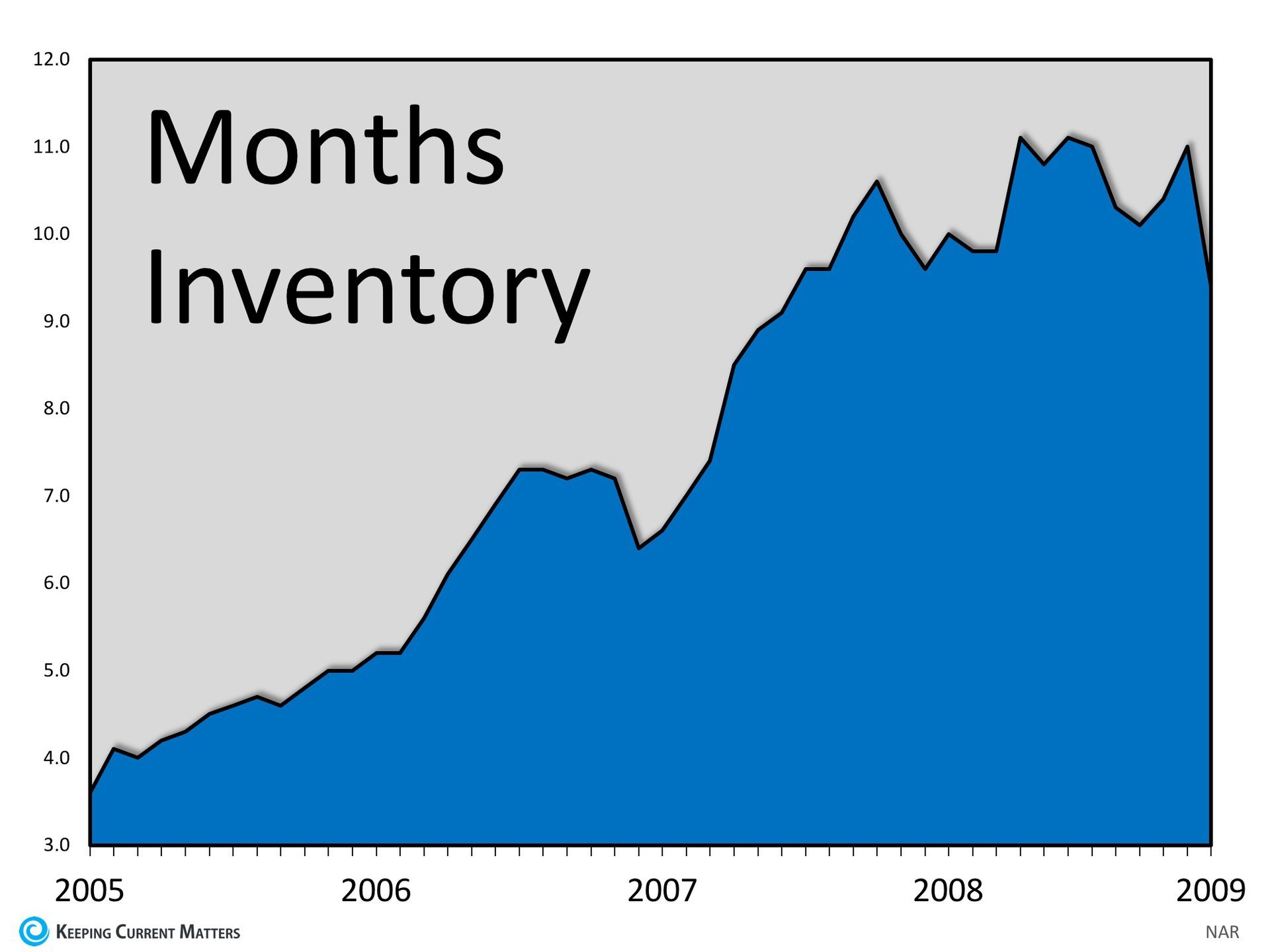

However, there is a major difference between the two markets. Last decade, while demand was being artificially created by extremely loose lending standards, a tremendous amount of inventory was coming to the market to satisfy that demand. Below is a graph of the inventory of homes available for sale leading up to the 2008 crash.

A normal market should have approximately 6 months supply of housing inventory. As we can see, that number jumped to over 11 months supply leading up to the housing crisis. When questionable mortgage practices ceased, and demand dried up, there was a glut of inventory on the market which caused prices to drop as there was too much supply and not enough demand.

Today is radically different!

There are those who believe that low mortgage rates have created an artificial demand in the current market. They fear that if mortgage rates continue to rise, some of the current demand will dry up (which is a possibility).

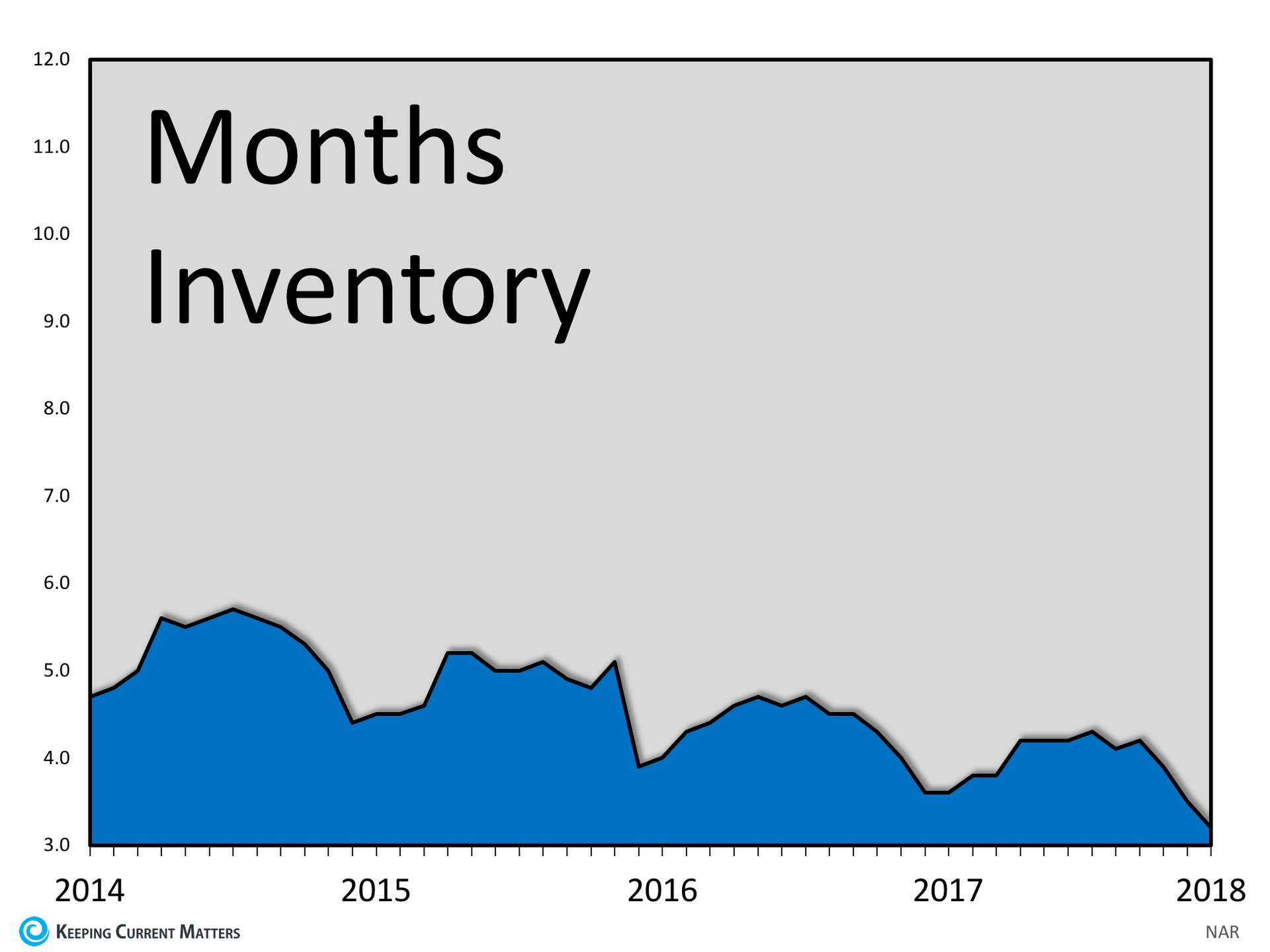

However, if we look at supply again, we can see that the current supply of homes is well below the norm of 6 months.

Bottom Line

We will not have a glut of inventory like we did back in 2008 and home values won’t come tumbling down. Instead, if demand weakens, we will return to a normal market (approximately a 6-month supply) with historic levels of appreciation (3.6% annually).

by Sharron Parker | Aug 6, 2018 | Home Buyers

In a CNBC article, self-made millionaire David Bach explained that: “Buying a home is the escalator to wealth in America. Homeownership can also help you retire early, that is, if you pay your mortgage off.”

Bach suggests that homebuyers should, “Take out a 30-year mortgage, but with the intention of paying it off in 25, 20 or ideally, 15 years.”

How does he suggest you do this? Here’s the secret:

“…If you were paying $1,000 a month, now you’re going to make $1,100 payments every month. Inform the bank that you are doing this and that you want the extra $100 a month to be applied to the principal (not the interest).”

What will happen to your mortgage?

Bach explains that, “If you keep this up, you’ll wind up paying off your 30-year mortgage in about 25 years. Increase your monthly payment by 20 percent, and you’ll have that mortgage retired in about 22 years.”

Bottom Line

Whenever a well-respected millionaire gives investment advice, people usually clamor to hear it. This millionaire gave simple advice – buy a home and pay off your mortgage early so that you can retire sooner with the money you will have saved!

Who is David Bach?

Bach is a self-made millionaire who has written nine consecutive New York Times bestsellers. His book, “The Automatic Millionaire,” spent 31 weeks on the New York Times bestseller list. He is one of the only business authors in history to have four books simultaneously on the New York Times, Wall Street Journal, BusinessWeek and USA Today bestseller lists.

He has been a contributor to NBC’s Today Show, appearing more than 100 times, as well as a regular on ABC, CBS, Fox, CNBC, CNN, Yahoo, The View, and PBS. He has also been profiled in many major publications, including the New York Times, BusinessWeek, USA Today, People, Reader’s Digest, Time, Financial Times, Washington Post, the Wall Street Journal, Working Woman, Glamour, Family Circle, Redbook, Huffington Post, Business Insider, Investors’ Business Daily, and Forbes.