by Sharron Parker | Sep 19, 2018 | Mortgage-Lending

Rising home prices have been in the news a lot lately and much of the focus has been on whether home prices are accelerating too quickly, as well as how sustainable the growth in prices really is. One of the often-overlooked benefits of rising prices, however, is the impact that they have on a homeowner’s equity position.

Home equity is defined as the difference between the home’s fair market value and the outstanding balance of all liens (loans) on the property. While homeowners pay down their mortgages, the amount of equity they have in their homes climbs each time the value of their homes go up!

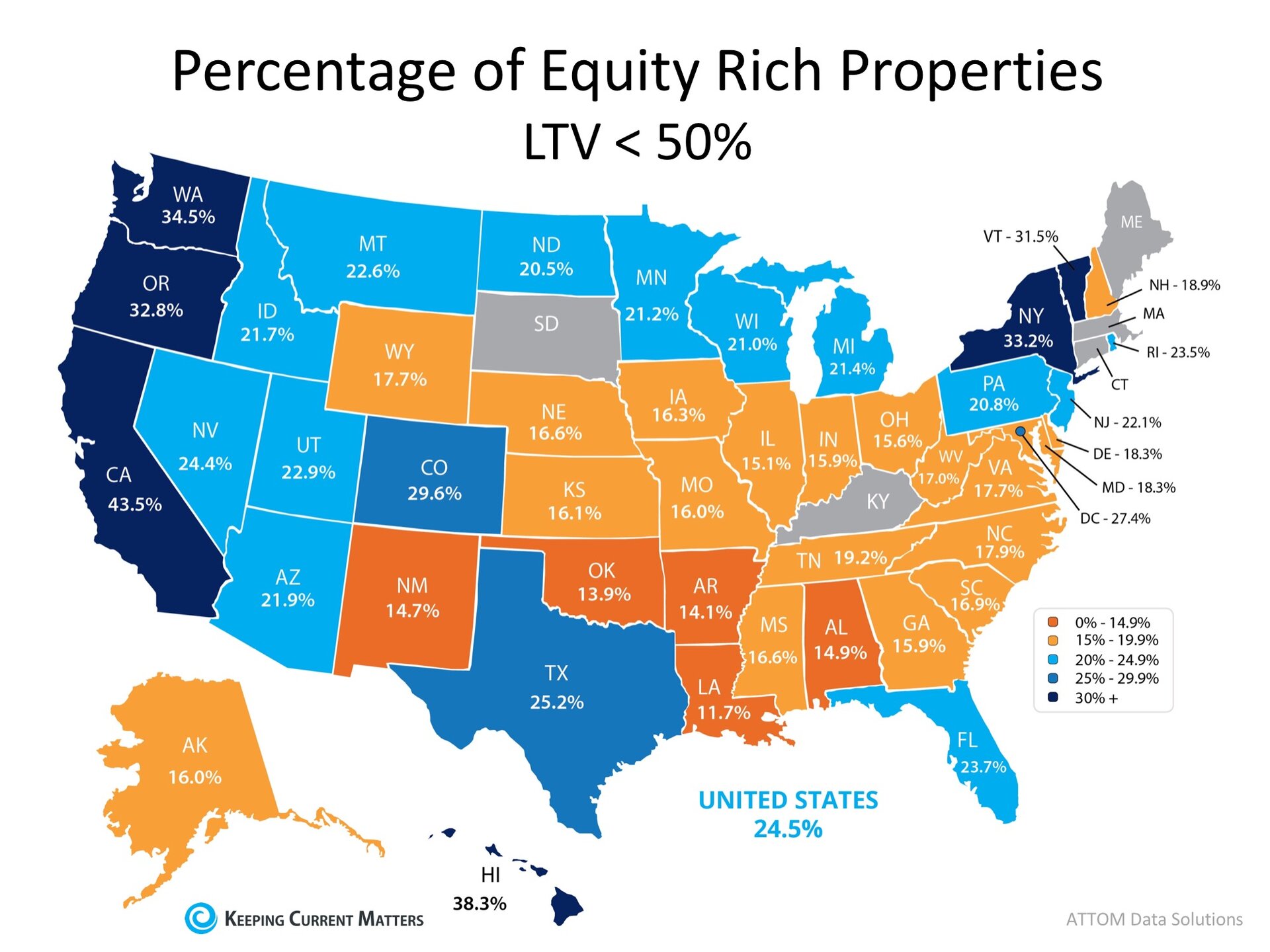

According to the latest Equity Report from ATTOM Data Solutions, “13.9 million U.S. properties in Q2 2018 were equity rich — where the combined estimated balance of loans secured by the property was 50 percent or less of the property’s estimated market value — representing 24.9% of all U.S. properties with a mortgage.”

This means that nearly a quarter of Americans who have a mortgage would be able to sell their homes and have a significant down payment toward their next home. Many who sell could also use their new-found equity to pay off high-interest credit cards or help children with tuition costs.

The map below shows the percentage of properties with a mortgage in each state that were equity rich in Q2 2018.

Bottom Line

If you are a homeowner looking to take advantage of your home equity by moving up to your dream home, contact an agent in your area to discuss your options!

by Sharron Parker | Jul 23, 2018 | Home Buyers, Mortgage-Lending

- Many buyers are purchasing a home with a down payment as little as 3%.

- You may already qualify for a loan, even if you don’t have perfect credit.

- Take advantage of the knowledge of your local professionals who are there to help you determine how much you can afford.

by Sharron Parker | Jun 14, 2018 | Housing Market, Interest Rates, Mortgage-Lending

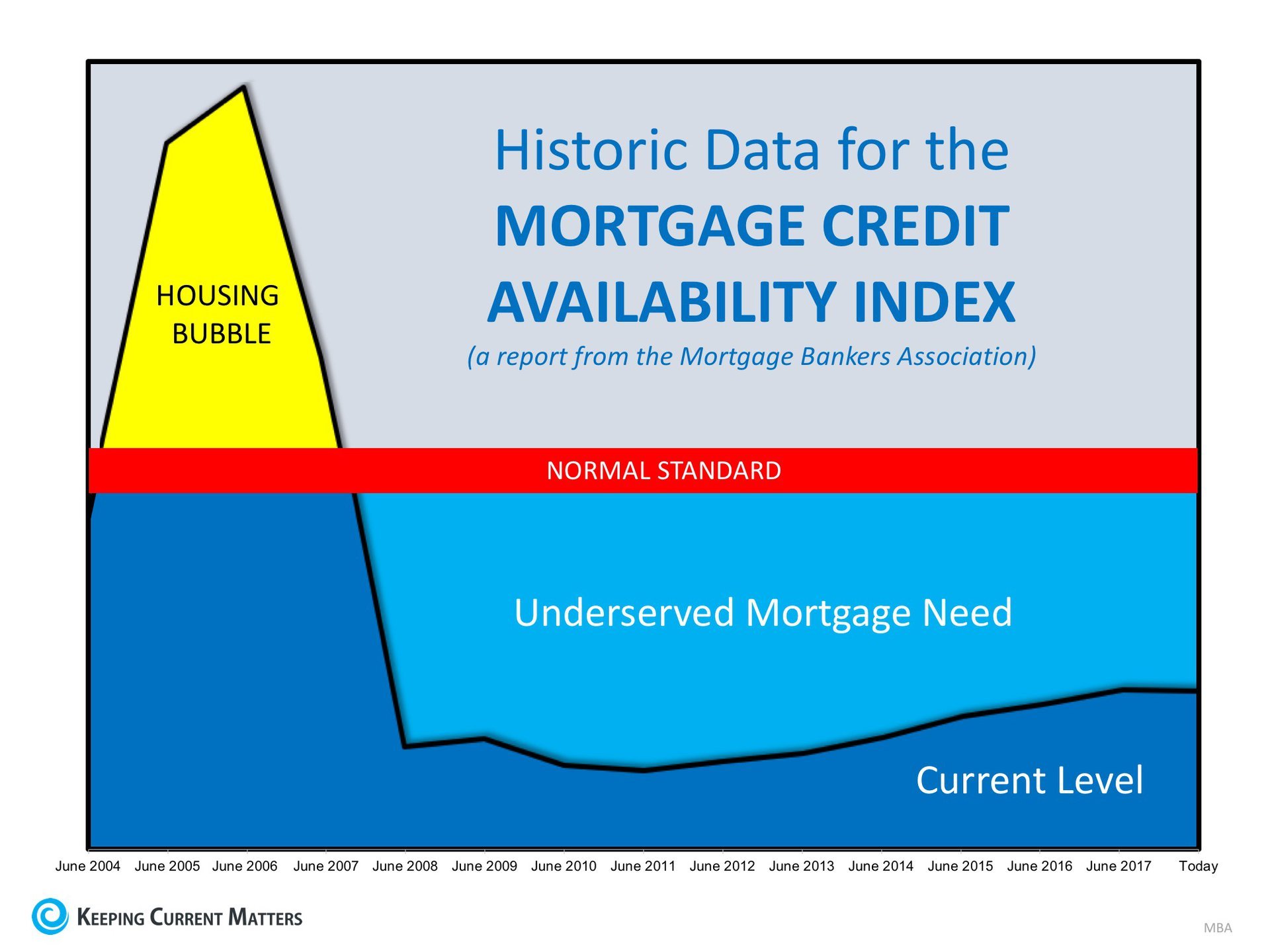

With home values appreciating at record rates, some are concerned that we may be heading for another housing bubble like the one we experienced a decade ago. One of the major culprits of that housing boom and bust was the loosening of standards for mortgage credit.

In a study done at the University of North Carolina immediately after the crisis, it was revealed that:

“Lenders began originating large numbers of high risk mortgages from around 2004 to 2007, and loans from those vintage years exhibited higher default rates than loans made either before or after.”

A study by John V Duca, John Muellbauer, and Anthony Murphy concluded that those risky mortgages caused the housing crisis:

“Our findings indicate that swings in credit standards played a major, if not the major, role in driving the recent boom and bust in US house prices.”

How do today’s mortgage standards compare to those from 2004 to 2007?

The Mortgage Bankers’ Association tracts mortgage standards in their Mortgage Credit Availability Index (MCAI). A decline in the MCAI indicates that lending standards are tightening, while increases in the index are indicative of loosening credit. While the chart below shows the index going back to that period between 2004 and 2007 when loose standards caused the housing bubble, we can see that, though the index has risen slightly over the last several years, we are nowhere near the standards that precipitated the housing crisis.

Bottom Line

If anything, standards today are too tight and are preventing some qualified buyers from getting the mortgage credit they deserve.

by Sharron Parker | May 31, 2018 | Housing Market, Interest Rates, Mortgage-Lending

Mortgage interest rates have increased by more than half of a point since the beginning of the year. They are projected to increase by an additional half of a point by year’s end. Because of this increase in rates, some are guessing that home prices will depreciate.

However, some prominent experts in the housing industry doubt that home values will be negatively impacted by the rise in rates.

Mark Fleming, First American’s Chief Economist:

“Understanding the resiliency of the housing market in a rising mortgage rate environment puts the likely rise in mortgage rates into perspective – they are unlikely to materially impact the housing market…

The driving force behind the increase are healthy economic conditions…The healthy economy encourages more homeownership demand and spurs household income growth, which increases consumer house-buying power. Mortgage rates are on the rise because of a stronger economy and our housing market is well positioned to adapt.”

Terry Loebs, Founder of Pulsenomics:

“Constrained home supply, persistent demand, very low unemployment, and steady economic growth have given a jolt to the near-term outlook for U.S. home prices. These conditions are overshadowing concerns that mortgage rate increases expected this year might quash the appetite of prospective home buyers.”

Laurie Goodman, Codirector of the Housing Finance Policy Center at the Urban Institute:

“Higher interest rates are generally positive for home prices, despite decreasing affordability…There were only three periods of prolonged higher rates in 1994, 2000, and the ‘taper tantrum’ in 2013. In each period, home price appreciation was robust.”

Industry reports are also calling for substantial home price appreciation this year. Here are three examples:

Bottom Line

As Freddie Mac reported earlier this year in their Insights Report, “Nowhere to go but up? How increasing mortgage rates could affect housing,”

“As mortgage rates increase, the demand for home purchases will likely remain strong relative to the constrained supply and continue to put upward pressure on home prices.”

by Sharron Parker | May 23, 2018 | Housing Market, Interest Rates, Mortgage-Lending

Interest rates for a 30-year fixed rate mortgage have climbed from 3.95% in the first week of January up to 4.61% last week, which marks a 7-year high according to Freddie Mac. The current pace of acceleration has been fueled by many factors.

Sam Khater, Freddie Mac’s Chief Economist, had this to say:

“Healthy consumer spending and higher commodity prices spooked bond markets and led to higher mortgage rates over the past week.

Not only are buyers facing higher borrowing costs, gas prices are currently at four-year highs just as we enter the important peak home sales season.”

But what do gas prices have to do with interest rates?

Investopedia explains the relationship like this:

“The price of oil and inflation are often seen as being connected in a cause-and-effect relationship. As oil prices move up or down, inflation follows in the same direction.”

You may have noticed that filling your gas tank has become substantially more expensive in recent months. The average national gas price has climbed nearly $0.50 from the beginning of the year, leading to the highest price for Memorial Day weekend since 2014.

As rates go up, your purchasing power goes down, but don’t worry; rates are still well below the averages we’ve seen over the last four decades.

“Freddie Mac said this year’s higher rates have not yet caused much of a ripple in the strong demand levels for buying a home seen in most markets, but inflationary pressures and the prospect of rates approaching 5 percent could begin to hit the psyche of some prospective buyers.”

Buying sooner rather than later will help lock in a lower rate than waiting, as the experts believe rates will continue to climb. Even a small increase in interest rates can have a big impact on your monthly housing cost.

Bottom Line

If you are planning on buying a home this year, keep an eye on gas prices the next time you’re at the pump. If you start to feel a big jump in price, know that rates are probably on their way up too.

by Sharron Parker | May 22, 2018 | Home Buyers, Housing Market, Interest Rates, Mortgage-Lending

According to Freddie Mac’s latest Primary Mortgage Market Survey, interest rates for a 30-year fixed rate mortgage are currently at 4.61%, which is still near record lows in comparison to recent history!

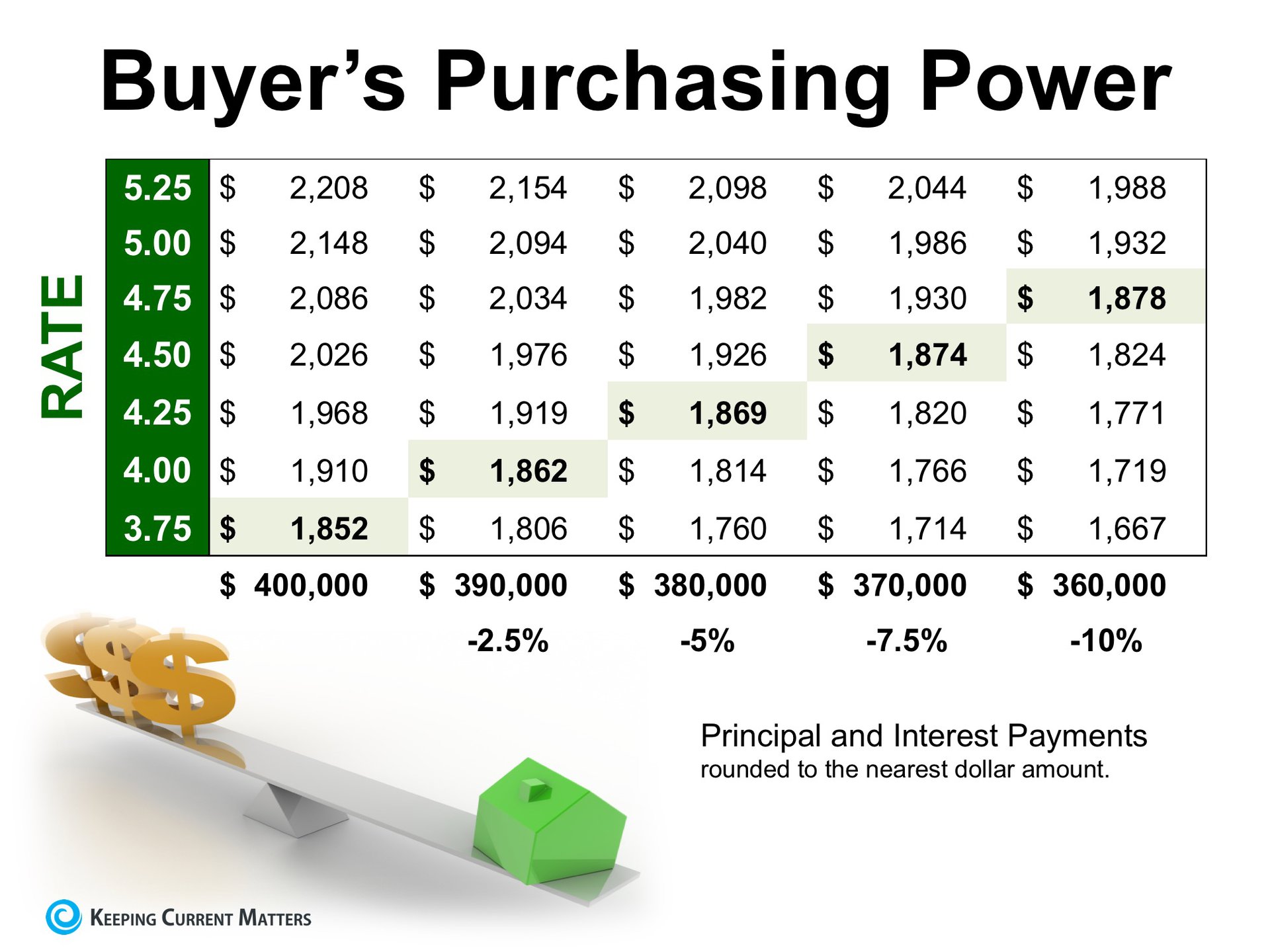

The interest rate you secure when buying a home not only greatly impacts your monthly housing costs, but also impacts your purchasing power.

Purchasing power, simply put, is the amount of home you can afford to buy for the budget you have available to spend. As rates increase, the price of the house you can afford to buy will decrease if you plan to stay within a certain monthly housing budget.

The chart below shows the impact that rising interest rates would have if you planned to purchase a home within the national median price range while keeping your principal and interest payments between $1,850-$1,900 a month.

With each quarter of a percent increase in interest rate, the value of the home you can afford decreases by 2.5% (in this example, $10,000). Experts predict that mortgage rates will be closer to 5% by this time next year.

Act now to get the most house for your hard-earned money.